Real Estate – Tax Benefits Guide – updated 1.4.2018

President Donald Trump signed into law the ‘Tax Cuts and Jobs Act 2018,’ effective 1.1.2018 and set to expire in 2025. This is the most substantial tax reform since the 1986 Tax Reform Act. It took two years to prepare and pass the 1986 Act. But it only took six weeks for the new 2018 Tax Reform Act. This post attempts to incorporate the latest tax law changes. Sign up for blog updates to learn about additional changes coming in the future.

Here we dive deep exploring a broad range of additional tax benefits of owning real estate. These real estate tax benefits apply anywhere in the United States, with the exception of a few additional Hawaii state specific tax benefits. The enclosed sample calculations use typical Honolulu property values that could be high, or low, compared to home values in your part of the country. Some of the numbers may need to be adjusted to fit your specific situation.

Taxes are hard to understand, calculate, and are subject to change. Always verify with your favorite qualified tax professional. My goal is to inspire further research and to help you prosper by making wise real estate investment decisions so that you may benefit from this new knowledge for the rest of your life.

$$$$$

Tax benefits fall into the following four basic categories:

a) Tax Deductions are expenses that are deductible against your taxable income, thus reducing your taxable income. The value of the tax deductions depend on your marginal tax rate.

b) Tax Credits are applied directly against your tax liability dollar-for-dollar, and thus are more valuable than deductions in reducing your tax liability. Tax credits have the same dollar value for all taxpayers where the tax liability is equal or greater than the credit.

c) Tax Exemptions reduce or eliminate some of your tax obligations, meaning being free from, or not subject to, taxation.

d) Tax Deferral allows you to delay tax payments until a later time.

The actual usage of your property will make a big difference on the type and amount of tax benefits available to you. This chapter is organized into two sections: 1) Owner Occupant Tax Benefits – when you use your home primarily for your personal enjoyment, and, 2) Real Estate Investor Tax Benefits – when you use your property mostly as an investment to generate rental income. The dividing line between both categories can be thin. Sometimes a primary home gets turned into an investment property and vice versa. Small changes in property usage can have a significant impact on your tax bill. Let’s get started.

1) Owner Occupant Tax Benefits

These tax benefits are available when you use your property for your personal enjoyment. Qualifying properties are your main home, aka primary or principal residence (where you live most of the time), and your other personal residences, e.g., a 2nd home, or your vacation home, as long as you don’t rent it for more than 14 nights max.

As an owner occupant, you get to deduct the following three expenses on your annual U.S. Federal tax return on Schedule ‘A,’ itemized deductions:

1) Mortgage Interest Deduction: Sec. 11042-11045. (Changes to Schedule A, itemized deductions). Effective 1.1.2018, you may deduct mortgage interest paid during the tax year on new mortgage loans up to $750K. This is a change from the $1Mill cap before. Only for existing mortgages, you may continue to deduct mortgage interest up to $1Mill. As of 1.1.2018, you may no longer deduct ‘Home Equity Line Of Credit’ (HELOC) interest paid during the tax year, unless used to buy or improve investment property (Check below, 2. Real Estate Investor Tax Benefits).

Not everyone will take out a new mortgage for $750K, but if you do, you would be able to deduct up to $31,630 (with a 30y fixed @ 4.25% jumbo rate) lowering your taxable income by the same amount during the first year of ownership.

You may also deduct any mortgage late payment fees (if any) and any mortgage prepayment penalty in the tax year paid.

2) Property Tax Deduction: Sec 11042-11045. (Changes to Schedule A, itemized deductions). Effective 1.1.2018, you may deduct all property taxes in the tax year paid, but only up to a $10K limit for the aggregate amount of state, local, and property tax you paid during the tax year.

3) Mortgage Points Deduction: You get to deduct the upfront cost to obtain a purchase mortgage loan, aka mortgage points, for the purchase of your main home, in the tax year paid.

However, when you purchase a second home, not your main home, you may not deduct mortgage points in the year paid. Instead you must deduct them spread out over the life of the loan. Points paid to refinance your mortgage (regardless if your primary or 2nd home) are also deductible over the life of the loan.

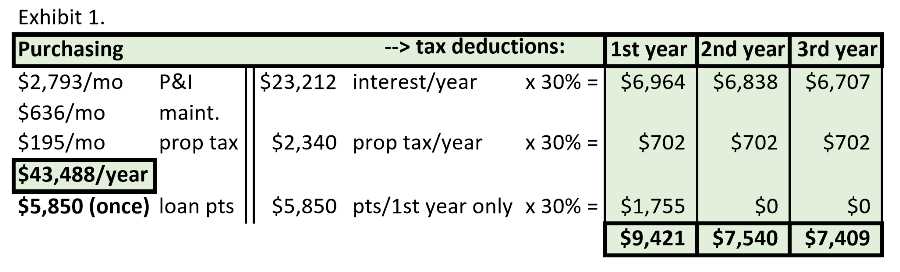

Sample tax calculation for an owner occupant purchasing a Honolulu condo:

Let’s assume you buy a Honolulu condo for sale at $650,000. An 80/10/10 owner-occupant loan program requires 10% or $65K cash down payment. The remaining $585K financed at 4% will cost $2,793/mo (principal and interest). You might also have to pay $636/mo maintenance fee (not tax deductible), and $195/mo property tax (tax deductible). To obtain the mortgage loan, you might pay one mortgage point (1% of loan amount = $5,850) loan funding fee at closing (tax deductible).

Total payments when purchasing: $3,624/mo (principal & interest & maint. & prop tax), or $43,488 a year, before tax deductions. Let’s not forget the one-time $5,850 loan funding fee.

Whether you know it or not, many of us easily pay a combined 30% or more in federal and state taxes (check Exhibit 2. below). For simplicity, we use the 30% bracket to calculate your potential tax savings on the three deductible expenses mentioned above. The formula is: Deductible expense x 30% = actual $ tax savings.

Exhibit 1. – In this scenario, you realize $9,421 in tax savings in the 1st year (full 12 months), and $7,540 in the 2nd year. The purpose of this blog post is simply to show the often overlooked tax savings. In another blog post ‘Wealth Creation With Real Estate’ we explore the long term financial implications of leveraging into Oahu Real Estate appreciating 4.5% annualized, compared to renting.

You might have been familiar with the above mentioned three deductions. However, there is more.

4) Mortgage Insurance – Tax Deduction: Private mortgage insurance premiums (to protect the lender), as well as FHA, VA and USDA mortgage insurance premiums paid by home buyers, have been tax deductible since 2007 as part of the 2006 Tax Relief and Health Care Act. The deductible amount has been subject to an income cap limit starting at $100,000.

5) Home Exemption – Property Tax Exemption: This one only applies to Hawaii. – Honolulu County property owners enjoy the lowest property tax rate in the nation: $3.50/y, per $1,000 assessed property value. A Home Exemption reduces your property tax. The exemption amount is deducted from the tax assessed value of your property, and you pay property tax only on the lower assessed balance. For your Hawaii principal residence only, you may claim the following home exemptions:

• Standard exemption: $80,000.

• Homeowner 65-years and older: $120,000.

• Hansen’s Disease, Blind, Deaf or Totally Disabled: $25,000, in addition to any exemption above.

• Disabled Veterans: Exempted from all property tax, except $300/y minimum property tax.

Note: This tax benefit is Honolulu County specific. Check with your tax adviser on property tax rates and exemptions available in your state / county.

You may qualify for your home exemption on your principal residence even if you are living in temporary accommodations away from your primary home up to two years because of a temporary work assignment, a sabbatical, or if your home was damaged due to a natural disaster.

6) Mortgage Credit Certificate, MCC – Tax Credit: (Tax update: As of 12.29.2017, this program is suspended but might get reinstated during 2018.)

This program is a first-time home buyer tax credit of 15% of your annual mortgage interest. Tax credits provide a dollar-for-dollar reduction against your federal tax liability, and you may still claim the remaining percentage of your mortgage interest tax deduction. The MCC can be applied to Conventional, VA, FHA, and USDA home loans.

7) First-Time Homebuyer – Penalty Free Retirement Account Withdrawals: The biggest hurdle for first-time home buyers often is the lack of cash funds for a down payment. The IRS allows you to withdraw $10,000, or $20,000 for couples, from your retirement account penalty-free for the purchase of your first home. IRA and SEP IRA withdrawal amounts are still taxable. ROTH IRA withdrawals are tax-free, but only if you opened your ROTH IRA more than five years ago. Other restrictions apply.

By the way, 401k withdrawals are taxable and do not enjoy the 10% penalty exemption. You could borrow against your 401k, up to half the account value but no more than $50K max. That would be a loan with interest that you will need to pay back.

Note: Before cashing in or borrowing against your retirement account, carefully evaluate all pros and cons with your favorite qualified professional retirement adviser.

8) Sec. 25D Renewable Energy – Tax Credit: You may claim a tax credit of 30% of the cost of renewable energy equipment that you install in your home. Qualifying renewal energy systems include solar panels, solar water heaters, geothermal heat pumps, wind turbines and some fuel cell equipment (with limitations). The credit amount is unlimited (!). You may roll over any unused tax credit portion exceeding your current tax year liability and use against your subsequent tax year liability.

This one is huge! Take advantage of this 30% upfront cost credited dollar for dollar, with a quick return on investment (ROI) for ongoing energy bill savings. The credit has been extended until 12/31/2021 (!). However, the 30% credit becomes a 26% credit in 2020 and a 22% credit in its last year 2021.

9) Sec. 25C Energy Efficiency Improvements – Tax Credit: You may claim a tax credit of 10% of the cost of some energy efficiency improvements to your home. Energy efficiency improvements may include the following: Electric heat pumps; Central AC; some qualified natural gas, propane or oil water heaters and furnaces; insulation and certain insulating roofs reducing heat loss or gain; insulating exterior windows, skylights, or doors, etc. Restrictions apply, including a lifetime credit limit of $500.

10) Septic Tank – Tax Credit: In Hawaii, Act 120 allows you to claim up to a $10,000 tax credit for the cost to replace each qualified cesspool with a septic tank, or a connection to the sewer system. This tax credit is available as of 1/1/2016 and expires 12/31/2020. There is a $5Mill total cap for each tax year. If you are unable to claim the credit in the current tax year, you may apply the credit in subsequent tax years up to 2020.

11) Home Improvements – Tax Deduction: Any improvements you make to your home are not directly deductible in the year the improvements are done, except as outlined in Sec. 25C, see paragraph 9.) above. You may, however, add the cost of these improvements to your cost basis which might diminish your capital gains tax at the time you sell your home. Make sure to keep accurate records of all your improvement expenses.

12) Short-Sale Mortgage Debt Forgiveness – Tax Exemption: Distressed homeowners selling their home as a ‘short-sale’ are exempt from paying tax on phantom income on the forgiven mortgage debt. This tax relief for homeowners with underwater mortgages has been in effect since 2007.

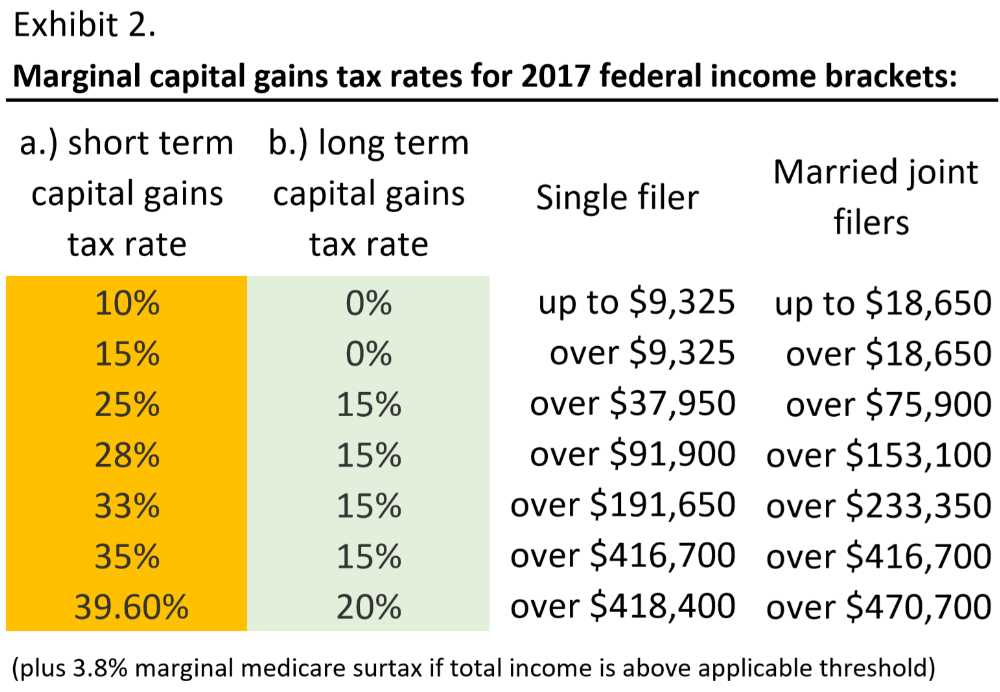

13) Sec. 121 Capital Gains Exclusion – Tax Exemption: Thanks to William Jefferson Clinton’s Taxpayer Relief Act 1997, individual homeowners are exempt from paying capital gains tax on up to $250K in gains at the time of sale of their principal residence. Married couples are exempt from paying capital gains tax on up to an impressive $500K in gains. Any gains exceeding the maximum exclusion amount are subject to the respective capital gains tax bracket based on your income level (see Exhibit 2. below).

You must have lived in your principal residence for two years out of the last five years before selling. This is an incredible gift horse opportunity and one of the largest, most generous tax breaks available to homeowners. The 2018 Tax Reform Act kept the original 1997 Tax Act provision unchanged.

Example: Let’s say five years ago you and your spouse bought your principal residence for $700K. With a) some sweat equity, b) smart value-added improvements, and c) increased property values, the home is now worth $1.2Mill. You and your spouse may sell your home at $1.2Mill without any capital gains taxes due. That is a whopping $500K tax-free money you can spend, invest, take a trip around the world, or buy another home and do it all over again. How sweet it is.

A) You may claim this exemption only once every 24 months, but as often as you like during your lifetime with every primary home you occupy two out of five years. I know clients that have repeatedly used this strategy, successfully bought, renovated, and sold habitually every two years or so, while substantially adding to their net worth each time.

B) The two years out of five years do not have to be the final two years, nor do they have to be subsequent years. Means, you may rent out your primary residence up to three years after your last use as a primary residence. You still may claim the tax exemption up to the $250K / $500K capital gains exclusion limit (subject to any depreciation recapture, see further below), provided the ‘two out of five years’ rule is satisfied (Sec. 121 (b)(4)(C)(ii)(I).

C) If you are an unmarried couple living together in your principal residence two out of five years and getting married just before the sale, you may claim the higher $500K exemption now as a married couple at the time of sale. Either spouse may own the property, but both must have been occupying the home as their principal residence to qualify for the higher $500K exemption.

D) You may claim a partial prorated exemption at the time of sale if you occupied your principal residence for less than two out of five years, provided you need to sell for health reasons, change in employment, or other unforeseen circumstances (Sec. 121 (c)(2)(B).

Example: If you sold due to unforeseen circumstances after only 20 months (instead of 24 months) of use as principal residence, you are exempt from paying capital gains tax on up to $208,333 in gains for a single tax filer (20 : 24 x $250K maximum exclusion = $208,333 prorated exclusion)

E) If you are a member of the military and you are being deployed, you may still qualify for the full tax exemption even if you do not meet the 2-year use as principal residence requirement.

F) If your spouse passes away, you may claim the tax exemption up to the full $500K capital gains exclusion limit, provided both of you occupied the home as your principal residence and you sell the home within two years of the loss of your spouse. If you wait to sell past two years after your spouse passes away, you may claim the exemption only up to the lower $250K capital gains exclusion.

• Rental properties converted into your principal residence for two out of five years owning. It became a favorite tax loophole for wealthy real estate investors to turn their rental property into their primary residence, then sell and claim the capital gains tax exclusion. The 2008 Housing & Economic Recovery Act effective 1/1/2009 closed the loophole and significantly diminished the tax benefit of doing so. The following restrictions apply today:

a) Sec. 121(d)(6): You may not claim a capital gains exemption for any gains realized by way of depreciation since May 6, 1997. (Depreciation recapture is taxed at your ordinary income tax rate, but capped at a top 25% rate, see paragraph. 22.)

b) Sec. 121(b)(4): After January 1, 2009, you may claim the capital gains tax exemption only for the time you used the property as your primary residence. Any time after 1/1/2009 that you did not use the property as your primary residence is considered ‘nonqualifying use’ (except up to three years after your last use as a primary residence, see C.) above). You may claim the capital gains tax exemption prorated over the holding period only for the years you used the property as your principal residence after 1/1/2009, but you may claim the full capital gains tax exemption for all years you owned the property before 2009, even if you rented it (!). Any use before 2009, even rental use, does not count as nonqualifying use. (Depreciation recapture tax still does apply).

Example: You bought your home as a married couple early Jan 2001 at $300K and sold early Jan 2016 at $700K with a $400K total gain (other than by way of depreciation) over 15 years. (For simplicity closing costs are not calculated). It has been your principal residence from 2001 through 2005 (5 years) and from 2014 through 2015 (2 years), but you did rent out your home from 2006 through 2013 (8 years). You may only claim the capital gains tax exemption for years 2001 through 2008 (8 years, until the law changed) and for years 2014 through 2015 (2 years) for a total of (8+2=) ten years prorated out of 15 years total holding period. $400K gains : 15 years = $26,667 x 10 years = $266,667 prorated gain exempt from capital gains tax. The remaining $133,333 gain is subject to capital gains tax at the applicable long-term tax rate (see Exhibit 2.). Note: Depreciation recapture tax does apply (see paragraph 22.).

• Rental properties converted into your principal residence after a 1031 Exchange.

To mitigate abuse of the Sec. 121 provision by wealthy real estate investors doing 1031 exchanges, the 2004 American Jobs Creation Act further restricts:

c) Sec. 121(d): If your rental property was part of a 1031 Exchange before turning into your principal residence, you might claim any capital gains tax exemption (subject to the above limitations) only after you held the property five years since the 1031 exchange.

— Homeowners have it good, but real estate investors take home the grand prize when it comes to tax benefits. In Chapter 28 we discussed how the cumulative effect of Cash Flow, Tax Benefits, Appreciation, Equity Pay Down, Forcing Equity, and Buying On Discount, compounded over time could create enormous wealth for wise real estate investors. My goal is to help you discover why investing in U.S. real estate has been favored by many. Here we focus on the multitude of tax benefits for real estate investors. All deductions and credits are against your gross income before your exemptions and standard deductions.

2) Real Estate Investor Tax Benefits

These tax benefits are available when you use your property as an investment. Qualifying properties are other than personal residences, e.g., rental properties generating income. The IRS considers rental property activity a business. You must report all rental income, but substantial tax benefits are available, provided you do not use the property for your personal enjoyment for more than 14 nights max. Vacation homes where your personal enjoyment time exceeds 14 nights, or 10% of the number of nights you rent out your home, whichever is greater, are considered personal residence, and you may not deduct the rental losses. You may, however, still deduct rental expenses up to the level of rental income, including property taxes and mortgage interest. Restrictions apply. Note: Renting your property to family or friends could jeopardize these tax benefits.

The following six tax benefits have already been discussed and are available as Owner Occupant Tax Benefits, but are also available for real estate investors:

• Mortgage Interest Deduction (for investment properties the entire interest expense is deductible without the $750K loan amount limit); HELOC interest paid on investment properties is also deductible if the HELOC proceeds are used for investment properties and not for personal use.

• Property Tax Deduction (for investment properties, the entire property tax expense is deductible without the $10K limit)

• Mortgage Points Deduction, deductible only over the life of the loan, rather than deductible in the year paid (as owner occupants are allowed to do)

• Renewable Energy – Tax Credit

• Energy Efficiency – Tax Credit

• Septic Tank – Tax Credit

In addition to these, the list of tax benefits for real estate investors continues:

1) Real Property Depreciation – Tax Deduction: This one is huge! Starting from the date your property is ‘placed in service’ ready to be rented, you get to depreciate the value of the improvements over the next 27.5 years for residential investment properties or 39 years for commercial properties. Improvements are any buildings or structures, e.g., houses, duplexes, condominiums, apartment buildings, parking garages, mobile homes, storage buildings, swimming pools, parking lots, tennis courts, clubhouses, walls, etc. Basically, any real property other than the land underneath.

Example: Let’s say you purchase a rental condo for $650,000. The value of the improvements might be $610,000, the value of the land might be $40,000. You get to deduct $22,182 depreciation per full tax year ($610,000 : 27.5y = $22,182) on your Federal tax return until you have entirely depreciated the improvement value after 27.5 years. A whopping $610,000 in deductions over 27.5 years, even though there is no actual loss in value.

But it gets better. Let’s say your rental produces $2,550 in monthly rent. A total of $30,600 in annual rental income, minus $22,182 annual depreciation equals $8,418. After your mortgage interest deduction and any other deductions mentioned in this chapter, your rental property might show a ‘paper loss’ on your tax return, lowering your overall tax bill while still enjoying a nice positive cash flow. That means your positive cash flow might not be taxable since the depreciation deduction could offset the profit. Pretty cool, passive income without paying taxes.

To determine the improvement value for your calculation, use the tax assessment record first to establish the ratio between improvement value vs. total value. Your tax assessed value might be different than the actual market value, or the price you paid, but once you have the correct ratio (improvement value : total value = ratio), then you can calculate the improvement based on your purchase price to use for your real property depreciation.

Remember, as a real estate investor you own an asset that over time may increase (appreciate) in value, and you get to depreciate the entire value of improvements on your tax return. Think about it, after 27.5 years, if maintained well, your rental property could produce even more rent and might also be more valuable, even though you have deducted the entire improvement value over the last 27.5 years. What other asset class provides this enormous dual benefit? How sweet it is to own real estate.

2) Personal Property Depreciation – Tax Deduction: When purchasing an investment property, some of the inclusions with the sale may be considered personal property rather than real property. Tangible personal property that lasts for more than one year might include appliances, e.g., washer, dryer, refrigerator, stove, dishwasher but also furniture, carpets, and even lawn mowers, etc. used for your rental business. Personal property you may depreciate faster, usually over five years rather than over 27.5 years. To depreciate over five years any personal property that was included with the real estate purchase, you will need to exclude the cost of these items from the property value basis that you are depreciating over 27.5 years. More on rental property depreciation here.

3) Repairs – Tax Deduction: All costs for ordinary and necessary repairs and maintenance to your property including the needed supplies may be fully deducted in the single tax year you incurred the expense. Deductible repairs and maintenance may include fixing plumbing leaks, snaking clogged sewer lines, re-painting, replacing broken windows, etc.

The IRS differentiates between repairs – deductible in a single tax year, versus improvements – depreciated over several years. Maximize your allowable deductions by doing repairs instead of improvements.

Note: Although repairs have an immediate tax benefit, repairs don’t necessarily improve the property value. Therefore a repair is still a net expense even after tax deduction. In contrast, capital improvements have two benefits: a) an increase in property value, and b) an increased cost basis for a reduced tax bill at the time of sale.

4) Improvements – Tax Deduction: Improvements to the property, rather than repairs, are for the Betterment, Adaptation or Restoration of the property, best to be remembered with the acronym ‘BAR.’ Improvements could include additions to the property, replacement or restoration of existing property components, or the adaption of the property to a new or different use. While you may deduct repairs immediately, improvements will need to depreciate over several years. For example, you may fully deduct a roof repair the same year, vs. a complete roof replacement, an improvement, which you may depreciate over time. The length of time to depreciate depends on the useful life expectancy of the improvement, more in IRS Publication 527.

5) Maintenance & Association Fees – Tax Deduction: You may fully deduct all condo maintenance fees and association fees in the tax year paid.

6) Property Management – Tax Deduction: A property manager might be charging you to handle the tenant screening, rent collection, check-in and check-out procedures. You may fully deduct all property management fees in the tax year paid.

7) Cleaning & Maintenance – Tax Deduction: Cleaning and maintenance might include cleaning fees, pressure washing, yard service, pool service, pest control service, etc. You may fully deduct these in the tax year paid.

8) Legal & Professional Services – Tax Deduction: Legal and professional services might include attorney fees, eviction costs, accountant fees, tax preparation fees, inspection fees, appraisal fees, real estate consulting fees, etc. You may fully deduct these in the tax year paid.

9) Utilities – Tax Deduction: If you pay for the property utilities, e.g., water, sewer, electricity, internet, etc., you may fully deduct these in the tax year paid.

10) Insurance – Tax Deduction: You may deduct the insurance premium paid for liability insurance, HO6 policy, RCUP rental condo unit owner policy, fire, flood, hurricane, tornado, earthquake, and other property insurance in the tax year paid.

11) GET, TAT & OTAT – Tax Deduction: Hawaii state specific, gross rental income received from rental properties on the island of Oahu is subject to 4.5% GET (General Excise Tax). If the rental term is less than 180 days, the gross rent received is subject to an additional 10.25% TAT (Transient Accommodation Tax), plus 3% OTAT (Oahu Transient Accommodation Tax for the city & county of Honolulu). You may deduct all GET, TAT & OTAT paid on Oahu gross rental income in the tax year paid.

12) Lease Rent – Tax Deduction: With Leasehold properties, Leasehold owners make regular monthly ‘ground lease’ rent payments to the landowner. Leasehold rent payments on investment properties might be tax deductible. Purchasing the ‘Fee interest’, meaning converting the property from Leasehold to Fee Simple, is not tax deductible.

13) Miscellaneous – Tax Deduction: You may also deduct advertising costs if you advertise your property for rent. You may deduct bank fees for tenant trust accounts, and you may deduct other regular business and office expenses as you would be able to deduct with any small business. After all, rental property activity is a business.

Besides the mortgage interest deduction on loans used to acquire or improve rental property discussed earlier, you may also deduct your credit card interest for goods and services used in a rental activity. More on rental property interest deductions here.

14) Travel expenses – Tax Deduction: As a landlord, you may deduct travel expenses to get to your rental property or even the trip to the hardware store to get material for a rental property repair. You may deduct your travel expense either by a) deducting your actual vehicle expense (gas, repairs maintenance), or b) you may use the standard mileage rate deduction. The standard mileage rate changes every year and is 53.5 cents/mile for the 2017 tax year and increases to 54.5 cents/mile for the 2018 tax year. You must keep accurate records of your miles. More on landlord car expense deductions here.

15) Long Distance Travel Expenses – Tax Deduction: As a long distance landlord you may even deduct the cost of your airfare, train or bus fare, rental car, hotel accommodations and even 50% of meals, provided the trip is primarily for your rental activity business. Rental activity business includes dealing with tenants, repairs, improvements, marketing, meeting with real estate attorneys, accountants, and real estate professionals. Travel expenses must be ordinary and necessary for you to conduct your rental activity business. Other restrictions apply. Bonus: You may even use your investment property up to 14 nights for personal enjoyment per year, but during your trip, your rental business activity days must outnumber your personal enjoyment days. Make sure you keep impeccable records of all your activities and expenses. More about long-distance travel expenses here.

16) Commercial Leasehold Improvements Accelerated Depreciation – Tax Deduction: You may depreciate qualified non-residential commercial leasehold improvements over an accelerated 15-year cost recovery period, rather than the regular depreciation timetable, see paragraph 1) above. This provision is now permanent with the Dec 2015 tax extender package

17) Sec. 179 Real Estate Business Equipment – Tax Deduction: (Sec. 13101 modifies Sec. 179 effective 1.1.2018) As a landlord and real estate investor, similar to any small business owner, you may immediately deduct new business equipment expenses. For example, you may expense computers, software, copiers, cameras, etc., up to a $1Mill(!) annual limit indexed for inflation, rather than depreciate equipment over several years. You may not need that many computers or copiers, but if you own a commercial building or restaurant business that needs a new build-out, you will welcome the generous annual limit. The business equipment must be brand new, meaning you are the first owner to place the equipment in service. You may deduct these items in the first year regardless if you are a sole proprietor, a corporation or an LLC. You may even deduct your new business vehicle in the first year if it is indeed used for business only. That does not apply to leased vehicles since you don’t own them. Also excluded is real estate, resale inventory, and property bought from a close relative. Sec. 179 deductions may not exceed your total taxable earnings. Other restrictions apply.

The 2018 Tax Act increased the old $500K amount effective 1.1.2018 to $1Mill aggregate cost deductions. The modified Act allows you to immediately deduct the improvement cost to non-residential real property, means commercial properties, but also lodging businesses such as dormitories and Airbnb. Improvements include new roofs, HVAC systems, fire protection and alarm systems, and security systems. The 2018 Tax Act also increased the phase-out threshold of Sec 179 expensing from $2Mill to now $2.5Mill.

18) Home Office – Tax Deduction: As a landlord and real estate investor, similar to any small business owner, you may claim a home office deduction. You may deduct home office expenses equal to the proportionate size your dedicated home office takes up compared to your total home size. Your home office must be used regularly and exclusively for your business. Home office deductions may include proportionate mortgage payments, taxes, and insurance, utility payments, phone, internet, etc., and must be related to your home office. You may not double deduct (!), e.g., your mortgage deduction and property taxes for your principal home and again for your home office. Accurately establish your home office size versus your home size. Restrictions apply and home office deductions can be red flags for IRS audits. Make sure to keep meticulous records.

19) Sec. 45L New-Home Energy Efficiency – Tax Credit: If you are not just a real estate investor, but a real estate developer or a new-home builder, you may claim a $2,000 tax credit for building energy efficient residences exceeding energy standards (heating and cooling) by 50%.

20) Sec. 179D Energy Efficient Commercial Buildings – Tax Deduction: If you own commercial real estate and or multifamily apartment buildings, you may deduct up to $1.80 per square foot if the building exceeds energy efficiency requirements under ASHRAE 2007. Restrictions apply.

21) Property Loss – Tax Deduction: If your investment property suffers sudden damage or destruction from fire, flood, theft or vandalism, aka ‘casualty loss,’ you may claim a tax deduction depending on the extent of loss and if the loss was not covered by insurance. Restrictions apply.

22) Sec. 162 Capital Expenditure $2,500 De Minimis Safe Harbor Election – Tax Deduction: Effective 1.1.2016, if you elect the De Minimis Safe Harbor (also provides audit protection) when filing your taxes, you may deduct up to $2,500 per each item invoiced to acquire, improve or produce tangible real or personal property for your real estate rental business. The threshold amount was increased from $500 to $2,500 as an administrative convenience with IRS Notice 2015-82. Wow, this one is huge! Think about it. If you need to purchase a dozen new refrigerators at $800 each for your dozen rental properties, you may deduct all of them in the tax year bought, provided each show as a separate line item not to exceed $2,500 on the invoice.

23) Sec. 1031 Exchange – Tax Deferral: This is a powerful tool for savvy real estate investors! Any gain on the sale of investment property usually is subject to debilitating capital gains taxes plus the often overlooked depreciation recapture tax, unless you take advantage of a 1031 tax-deferred exchange, aka, Starker exchange.

To understand the tax savings, let’s look at current tax rates depending on the property’s holding period:

a) Gains on investment properties sold within one year of purchase are subject to short-term capital gains taxes, which is the same rate your ordinary income is taxed.

b) Gains on investment properties sold after one year of purchase are subject to long-term capital gains taxes, which is a much more favorable tax rate.

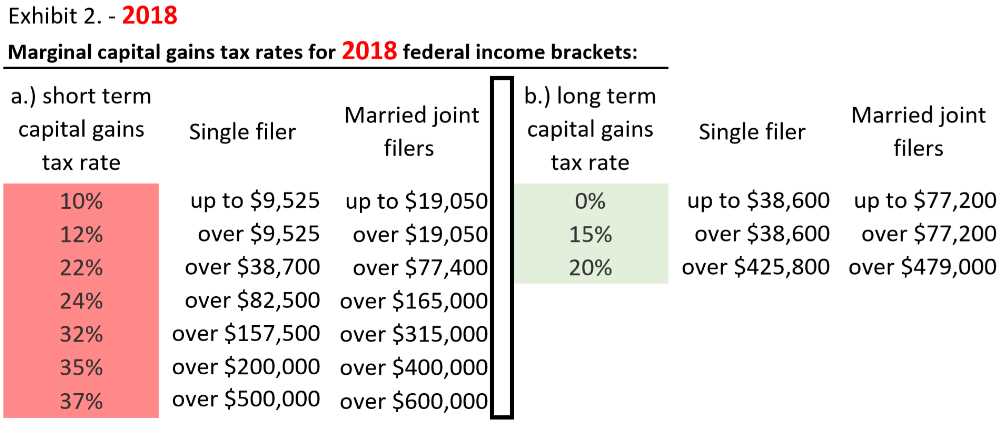

Exhibit 2.- 2018 – shows marginal capital gains tax rates: a.) short-term rate (same as your income tax rate), and b.) long-term rate, for respective 2018 income brackets, filing in 2019. (The 3.8% marginal Medicare surtax was eliminated effective 1.1.2018).

Besides capital gains tax, the depreciation recapture tax gets added to the tax bill. That is the tax on all the depreciation you deducted on your tax returns. The depreciation recapture is taxed at your ordinary income tax rate but is capped at a top 25% rate. Most likely it will be 25% for you, and not less.

In our depreciation example above, you depreciated $610,000 over 27.5 years. All of the depreciated $610,000 is subject to the recapture tax at the time of sale, at least up to the limit that you have gains on the sale of your property. This means if your gain at the time of sale is less than the amount you were able to depreciate over your holding period, than you may only pay recapture tax on the amount equal to the gain realized.

By the way, the recapture tax is applicable even if you failed to take the depreciation deduction! Double bummer. You can see that a big chunk of your gains can quickly disappear unless you know how to get around it by taking advantage of the ingenious 1031 exchange.

A properly structured 1031 exchange is one of the most excellent tools available for you as a real estate investor to build substantial real estate portfolios and long-term wealth by deferring both capital gains tax and the recapture tax!

With tax deferral, as a real estate investor you may re-balance your investment portfolio, improve cash flow, increase leverage, improve appreciation potential, trade up into better quality properties and reduce maintenance or management costs. An exchange may also create new depreciation deductions (see par 1.) to the degree of added value difference between both properties for an after-tax net cash flow benefit – a nice bonus if you already fully depreciated the relinquished property. You could be trading up via 1031 exchanges as often as you like, rolling your equity into ever bigger and better deals all while never paying the tax, unless a) you finally cash out, or b) until you die. Upon death, your real estate will be inherited by your heirs at the stepped-up basis eliminating both, all deferred capital gains and recapture tax.

Here are the basic 1031 exchange rules: As a real estate investor, you may defer capital gains tax and recapture tax by selling one or more investment properties and purchase one or more ‘like kind’ investment properties at equal or greater value. ‘Like kind’ means both the relinquished (sold) and replacement (bought) properties need to be investment properties (must show on your tax return schedule E) and must be located within the U.S. Disqualified are your principal residence and your 2nd home or vacation home.

After the sale and recordation of the relinquished property, you have a maximum of 45 days to identify one or several replacement properties and a maximum of 180 days to close on the replacement properties. A third party qualified intermediary is required to hold all sales proceeds in the interim and will prepare the exchange documents. You may also reverse the exchange order: buy first and sell second, aka, a reverse 1031 exchange.

1031 exchanges can be tricky, and additional rules and restrictions apply to qualify for successful tax deferral. Make sure you get all the fine details correct because a failed exchange could be detrimental to your financial growth.

24) Rental Income – Self-Employment Tax / FICA Tax Exemption: If you are self-employed, your earned income is usually subject to a 15.3% self-employment tax. If you are employed, the tax shows as FICA (Federal Insurance Contribution Act) on your W-2 form, which is the 15.3% split 50/50 between you and your employer.

The IRS does not treat rental income as earned income (except when RE income flows through a C-corp). Therefore, rental income is exempt from the self-employment / FICA tax. One more reason why collecting rent from your rental properties is better than earned income.

25) Flow-through small business 20% Deduction: Effective 1.1.2018, the new tax law allows certain businesses a 20% deduction. This deduction may apply to your Schedule E rental income. Income restrictions apply. This new deduction does not apply to interest, dividends, and capital gains income.

26) Sec. 469 Qualified Real Estate Professionals – Unlimited Tax Deduction: All above deductions, including the huge depreciation deduction, quickly amount to significant savings and could easily offset and exceed your rental income, making it virtually tax-free. Deductions and depreciation create sizable paper losses to offset a portion of your ordinary working income. Remember, paper losses are useful and reduce your overall tax obligation. The more, the better. Except, your allowable losses are limited to $25K per year for married couples filing jointly with up to $100K modified gross income. Allowable losses phase out above $150K modified gross income. But you may carry any unused losses including unused depreciation forward for years until you can, even until the day you sell your property! Then you may use all deferred paper losses to offset taxes and possibly eliminate the need to do a 1031 exchange. Nice!

But I saved the best for last. If you are truly ambitious and a dedicated real estate investor, the sky is the limit. Sec. 469 eliminates the $25K annual loss cap and allows you to claim unlimited paper losses! You may claim unlimited losses as a Qualified Real Estate Professional, but you must meet specific criteria:

• You must spend more hours in real estate activities on an annual basis than in any other business.

• You must be actively involved in real estate activity for a minimum of 750 hours per year.

As a married couple filing joint tax returns, either spouse may satisfy these requirements. You might be surprised to know that you do not have to be a licensed realtor. Qualified real estate activity includes real estate development, re-development, building, restoration, remodeling, buying and selling, converting, renting, managing and operating real estate.

Make sure you keep accurate records of time spent on your real estate activity versus the time you allocate to other business activity. Claiming Sec. 469 unlimited deductions often can be a red flag for IRS audits, and you will need to document and support your material involvement to justify your eligibility. Additional restrictions apply.

Hopefully we inspired you to delve further into real estate tax benefits. Also, check out this handy IRS page. Disclaimer: I’m a real estate investor and a licensed real estate broker. I completed many 1031 exchanges as well as assisted countless real estate investors with growing their respective real estate portfolios. I’m not a professional tax adviser. For tax matters always check with your favorite qualified tax professional.

We love to hear from you. – Please share, like and comment below.

Thank you for such a great article! To qualify for investment property, How to track or prove how many days I stayed at the property for personal entertainment?

Aloha Weili Geng!

We have no affiliation with the IRS, and we don’t vouch for what the IRS might consider ‘sufficient’ proof.

Just make sure your records are immaculate. Because splitting your property expenses on both Schedule E (investment use) and Schedule A (personal use) increases the risk of an IRS audit!

Check our related article:

https://www.hawaiiliving.com/blog/personal-use-hawaii-vacation-rental/

In doubt, always check with the IRS, or your favorite qualified tax professional.

Let us know when you, or anybody you know, is ready to buy or sell again. 🙂

We are delighted to help. ~ Mahalo & Aloha

Very well written. I really appreciate your hardwork.

Aloha Dipak Patel!

Thank you for your kind words. We are here to help.

Call us when you are ready to buy or sell more real estate again.

We are here to help.

Mahalo & Aloha

Aloha, great article…bookmarking this one forsure! I am a bit confused about the, “living in the home 2 out of the past 5 years” part. Does that mean i have to own the home for 5 year? Or, can I just own it and live in it for 2 years?

Aloha Trevor Sawyer! Thank you for checking in.

Owning and living in it as your primary residence for 2 years is sufficient, except:

— If your property was bought as part of a 1031 Exchange before turning into your principal residence for 2 years . Then you may claim a capital gains tax exemption only after you held the property five years since the 1031 exchange [Sec. 121(d)].

— Also, if you owned the property for 5 years, the two years out of five years do not have to be the final two years, nor do they have to be subsequent years. Means, you may rent out your primary residence up to three years after your last use as a primary residence. You still may claim the tax exemption up to the $250K / $500K capital gains exclusion limit (subject to any depreciation recapture as mentioned in the article), provided the ‘two out of five years’ rule is satisfied [Sec. 121 (b)(4)(C)(ii)(I)].

— Always check with your favorite qualified tax professional and contact us when you are ready to buy or sell. 🙂

~Mahalo & Aloha

ALOHA again,

Looking at all the incredible information, I do have a quick question. HOTEL/CONDO is what I am interested in. I looked at some examples of of 2016 stats for i.e. TRUMP towers vs. Palms. I am excepting of only using my condo 14 days a year for max tax deductions. If I want to use longer, am I eligible to go through the renting pool and rent back my condo to me/family so we can stay at a different time/longer? If I come in to do work on the condo on a separate occasion,I understand the tax deductions would be in my favor, but can I stay in my own condo while doing the repairs? Does that go against the original 14 day stay? Thanks for any information offered.

Does the state of HAWAII offer classes on island as mentioned below?

MAHALO

Lisa Lisa Rivaldo-Dillon

————————————————————-

Your Trip Must Be for Business

In order to deduct the cost of your trip, it must be primarily for your rental activity. This means that you must have a rental purpose in mind beforMAHAe starting out, and you must actually do something for your rental activity while you’re away. Examples of rental business purposes include:

traveling to your rental property to deal with tenants, maintenance, repairs, or improvements

traveling to building supply stores or other places to obtain materials and supplies for your rental activity

traveling to your rental property to show it to prospective tenants

learning new skills to help in your rental activity, by attending landlord-related classes, seminars, conventions, or trade shows, and

traveling to see people who can help you operate your rental activity, such as attorneys, accountants, or real estate brokers.

Aloha Lisa Rivaldo-Dillon!

Sorry for the delay, I don’t check here on a regular basis.

There are several glaring issues that I would like to clear up.

For the most excellent and effective service, call my cell 808-554-1635, or email: George@HawaiiLiving.com, with the best number to call you back.

We’ll get you up to speed, help answer your questions, and assist you with the purchase of the most fitting condo option.

We are here to help.

~ Mahalo & Aloha

Hello George,

I am learning so much about rental properties do’s and dont’s and thank you so much. But I need clarification about a paragraph which I have copied and pasted below. I want to buy a condo/hotel in a building where I can have a hotel chain manage it. But I want to be able to use my property several times a year. If I am reading what you posted it looks like I can only use it MAX 14 days a year? Is that correct? Any input is appreciated. Is there a an advantage to buying a unit cash vs. having a monthly payment if I want to use it more than 14 days? Thanks again,

Lisa

The IRS considers rental property activity a business. You must report all rental income, but substantial tax benefits are available, provided you do not use the property for your personal enjoyment for more than 14 nights max. Vacation homes where your personal enjoyment time exceeds 14 nights, or 10% of the number of nights you rent out your home, whichever is greater, are considered personal residence, and you may not deduct the rental losses. You may, however, still deduct rental expenses up to the level of rental income, including property taxes and mortgage interest.

Aloha Lisa Rivaldo-Dillon!

Thank you for your excellent question.

You are correct. To claim the massive tax deductions available to you as an investor, you may only use your investment property up to 14 nights per year, or 10% of the number of nights you rent per year.

If your ‘personal use’ exceeds the limit, then you compromise ‘most’ of your tax deductions, but not all of them. Check here for the details: https://www.hawaiiliving.com/blog/personal-use-hawaii-vacation-rental/

Cash or financed purchase does not change the 14 night rule. The mortgage interest deduction is available for both scenarios. The number of deductions that could be compromised are the ones listed above under 2) ‘Real Estate Investor Tax Benefits,’ excluding the first three benefits listed under 1) ‘Owner Occupant Tax Benefits.’

Let us know how we may assist you best. We don’t just write about this stuff. We are experts in client representation and we are here to help ready when you are.

~ Mahalo & Aloha

Thank you so much for your help and input. I am so tossed as what to do? I am in and out of hawaii about 7 times a year due to my job and would LOVE to stay at my own property. I guess I have to weight out the differences.

Mahalo, Aloha and have a great week. If you have any ideas let me know but it looks like the tax laws are specific.

Lisa Dillon 🙂

George Krischke, Principal Broker, Hawaii Living LLC

Hi George I love your whole article – – did you compose it all or is it from somewhere else? I’d love to copy it – but want to do it right..know what I mean?

Aloha Maria,

Mahalo for your kind words. It took about a month to organize and write this article. I’m commited to update as laws change. You may link to it anytime you like. Let me know if there is anything else you would like us to write about that might be useful. We are here to help. 🙂 ~ Mahalo & Aloha

George Krischke, Principal Broker, Hawaii Living LLC